The idea of finally retiring from work may fill some with joy – but it can also be a great source of anxiety. It is all well and good to dream of long summers, holiday homes and big family trips, but how much money do you need to fund a new life without a salary?

Ian Cook, of the wealth manager Quilter, said: “In days gone by, defined benefit pensions meant that people typically didn’t need to worry about their pension income running out because they got a guaranteed income for life.

“Now, in the world of defined contribution schemes , you need to carefully balance how much you want to have for your retirement and how long you want it to last for.”

Hereunder, Telegraph Money elucidates ways in which one can finance a comfortable retirement. It also highlights potential factors such as early retirement and the expenses associated with long-term care, suggesting that these may necessitate setting aside additional funds.

- What constitutes a comfortable retirement income in the UK?

- Ways to Boost Your Retirement Savings Pot

- Can you afford to retire early?

- Do your savings need a bigger boost?

- Comfortable retirement FAQs

What is a comfortable retirement income in the UK?

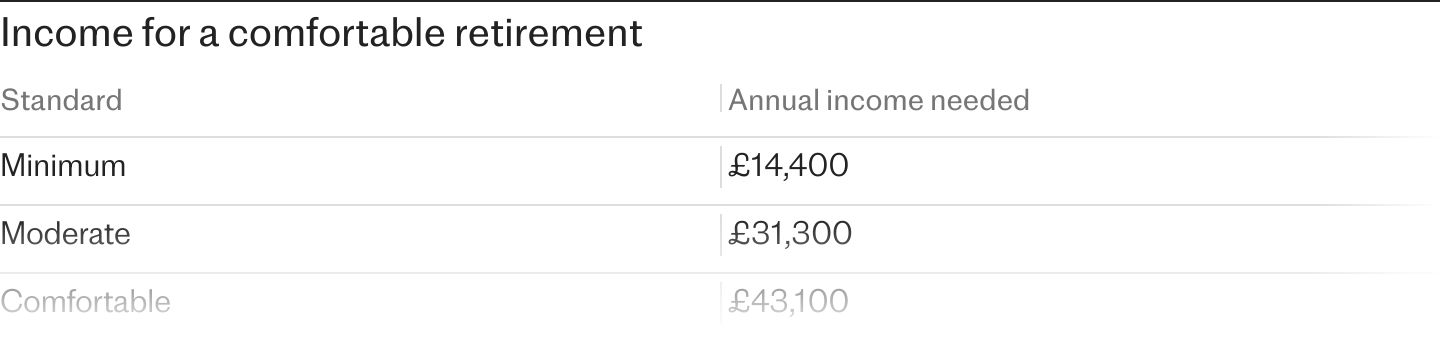

A “comfortable” retirement, according to the Pension and Lifetime Savings Association (PLSA), includes having the budget to stretch to luxuries such as regular beauty treatments, theatre trips and two weeks holiday in Europe every year, with around £130 to spend on groceries each week and £80 a week on meals out.

This, according to the research, is expected to cost around £59,000 for a couple, or £43,100 for a single person.

A “moderate” retirement, meanwhile, refers to a lifestyle where you can afford a few luxuries, including being able to take a week’s holiday in Europe and a long weekend in the UK each year, run a small second-hand car and buy occasional treats for yourself. You could spend £100 a week on groceries, and have a fund of £60 a week for eating out.

On a minimum income, however, PLSA estimates that you cannot afford a car and holiday in the UK instead, with smaller budgets for food, clothes and gifts.

The table below shows how much pension income experts think you need each year, depending on your lifestyle.

How to increase your retirement pot

These figures may not sound too far out of reach, but building up a pot big enough to consistently pay out these sums each year is not easy – especially as the overall value of your pension will fluctuate depending on moves in the stock and bond markets.

To help fund the retirement you seek, you should consider taking the following steps, which include plans for both your state and private pension:

- Check your state pension forecast – you can do this on gov.uk .

- Fill in gaps in your National Insurance record

- Increase pension contributions

- Maximise employer contributions to your workplace pension

- Consider opening a Sipp

- Make lump sum contributions

- Invest wisely

- Make the most of available tax relief

- Cut unnecessary expenditure by budgeting

- Use the full Isa allowance

The initial step should be reviewing your state pension projection, since these governmental payouts will serve as a valuable foundation for your retirement earnings.

You will be eligible for the complete amount. state pension If you've made 35 years' worth of National Insurance contributions, this can differ based on your work history — for instance, if you've ever been employed overseas, your record might be shorter. Therefore, it’s advisable to verify this ahead of time. You can obtain an official state pension forecast through the relevant service. government website .

Should there be breaks in your National Insurance history, you have the option to make up for them by paying voluntary contributions or claiming NIC credits to enhance your state pension entitlements. You now have until April 4th to complete any missing sections. from 2006-07 onwards.

Currently, the state pension age stands at 66; however, it’s gradually increasing to 67 by 2028, with plans set for another hike to 68 sometime around the mid-2040s. Should you wish to retire earlier than these ages, your financial strategy must include a significantly larger private or occupational pension to support such an early retirement plan.

Are you able to manage an early retirement?

It hinges on your specific situation, including your pension arrangements, savings, any debt obligations you may have, and how you envision your retirement lifestyle.

You can technically choose to “retire” and stop working at any age if you can afford it, but if you’re planning to live off your pension the earliest age at which most people can access their private pension pot is set at 55. This is meant to stay at around 10 years lower than the state pension age, and is due to increase to 57 in April 2028.

Our step-by-step guide to retiring early can help you prepare.

How much do I need to retire at 55?

As mentioned above, this depends on the kind of lifestyle you want to maintain throughout your retirement.

To fund a comfortable lifestyle, you would need a pension worth around £700,000 on top of your state pension, according to calculations by Quilter. That would leave you with around £78,690 by the time you reach the age of 82. If you lived beyond this, your pot would be exhausted by the time you reach 88.

The tables below show how retirement age affects the required size of pension pot.

Waiting for your state pension payments can alleviate some of the pressure. If you kept working until the current state pension age of 66, then your pot would need to be around £450,000.

It would be worth around £122,176 by the time you reached 84, at the average life expectancy. It is important to keep these figures in mind as anything left in your pension can be passed on free of inheritance tax.

See the tables below to see how much a moderate retirement costs when you retire early, versus working beyond state pension age.

Do your savings need a bigger boost?

There are several scenarios to consider that may indicate a need to boost your pension pot, including:

- Marriage or divorce

- Economic instability

- Unexpected health issues

- History of familial longevity

- Tax changes

Some people plan for retirement under the assumption that they will need less money as they age, because they will go out less and will have paid off any leftover debts – but this may not be true if you need help with care, Quilter’s Ian Cook added.

The “healthy” life expectancies of men and women are 63 and 64 years respectively, so you could feasibly need two decade’s worth of help if you live into your eighties.

Given all these cost pressures, your pension pot may look leaner than you would like. If this is the case, the key is not to panic as there are still lots of ways that you can help your nest egg grow, especially as the cap on lifetime pension savings is in the process of being dismantled.

The lifetime allowance

The lifetime allowance has been abolished. When it was in place, it capped the amount you were able to save – most recently at £1,073,100. If you exceeded this amount, you were subject to tax at a maximum of 55pc.

Mr Cook said: “During your lifetime you may have increases in your salary, big bonuses or a windfall from an inheritance or elsewhere. Whenever this happens, think about your pension.”

The annual allowance caps how much you can pay into your pension tax-free each year. It is set at £60,000, but tapers down for higher earners.

For people who have already retired and are considering a return to work, a different rule applies when paying into their pension – payments are subject to the “money purchase annual allowance” which is set at the lower level of £10,000.

Comfortable retirement FAQs

How much money does the average person have when retiring?

According to the latest figures from the Department for Work and Pensions , the average single pensioner has an income of £13,884 a year. For couples, that jumps to £29,172 between them. This is after housing costs.

See our guide to the average pension pot for more information.

How long will my money need to last?

This is difficult to know with any certainty, as no one really knows how long they are going to live.

You can make a plan based on the average life expectancy in the UK, which is 78.6 for men and 82.6 for women, according to the latest government figures .

If you were to take your pension at 55, then you would need it to last on average for around 25 years.

Should I retire abroad?

Escaping British weather for sunnier climes is a popular option, but there are extra factors to consider when retiring abroad, which could mean needing an even larger pot.

You are likely to need a visa and evidence that you can support yourself if retiring abroad in popular European Union countries, with each member state having its own minimum income requirements.

British pensioners also have to be careful when retiring to France or taking their pension in Spain as the 25pc tax-free withdrawals rule does not apply if accessing the funds while living in these countries. France and Spain also have a wealth tax, which could reduce your income.

In contrast, retiring in Portugal It might appeal more to individuals with substantial pensions because there’s no wealth tax, along with the added benefit of only paying 20% tax on foreign pension income.

Nobody can foresee the extent to which bills will increase or the effect that inflation and interest rates may have on your earnings irrespective of where you choose to retire. Thus, calculating the amount needed for your retirement is a complex issue; however, the straightforward solution might be—save as much as feasible.

Enjoy The Telegraph’s fantastic selection of Puzzles – getting smarter daily has never been more enjoyable. Challenge your mind and enhance your spirits with PlusWord, the Petite Crossword, the daunting Killer Sudoku, and yes, even the traditional Cryptic Crossword.